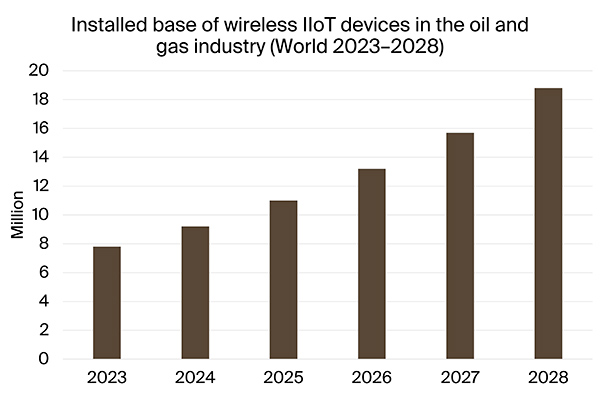

According to a new research report from the IoT analyst firm Berg Insight, the installed base of wireless devices featuring cellular, satellite or LPWA connectivity in the oil and gas industry is forecasted to grow at a compound annual growth rate (CAGR) of 19.3 percent from 7.8 million units at the end of 2023 to 18.8 million connected devices by 2028.

Remote monitoring of assets such as industrial equipment, tanks and pipeline infrastructure in the midstream and downstream sectors comprise the most common applications for wireless industrial IoT (IIoT) solutions in the oil and gas industry. The expected growth in cellular device shipments is attributed to a higher adoption rate of sensor applications based on LTE-M and NB-IoT technologies and continued preference for cellular communications in the remote tank monitoring segment. Since many remote monitoring applications have limited requirements on bandwidth, Berg Insight is of the opinion that non-3GPP LPWA technologies such as LoRa can achieve a significant position on this market as well.

Partnerships among industrial automation vendors and technology companies continue to be a theme in the oil and gas industry while expanding in scope with oil and gas operators and software companies. Global automation vendors including ABB, Emerson, Hitachi, Honeywell, Rockwell Automation, Schneider Electric, Siemens and Yokogawa can deliver complete solutions thanks to their extensive partner ecosystems.

In addition, the choice of preferred network topology and communications standards depends on the application area as each activity in the oil and gas value chain has its own specific need for connectivity. Many providers recognise the industry’s diverse needs by integrating different types of wireless capabilities into single box solutions. Connectivity providers such as Advantech, Cisco, HMS Networks, Moxa, MultiTech and Robustel offer modular routers and gateways where different wireless interfaces can be added to the device.

Wireless sensor solutions for remote asset monitoring are today offered with various options for communications such as LTE-M, LoRa and satellite. This suggests further convergence of wireless technologies and flexible offerings featuring hybrid solutions to serve the full range of connectivity needs in the oil and gas industry.

“Oil and gas companies are increasingly relying on data from IIoT devices to make better informed decisions”, said Veronika Barta, IoT Analyst at Berg Insight.

Today, IIoT devices can collect vast amounts of sensor data such as pressure, level, flow and temperature. As operators move towards more remote and autonomous operations, the need to collect greater volumes of data increases. The large data volumes call for edge processing capabilities to acquire data significance. In upstream applications, edge computing is used to collect and analyse real-time data from devices at drilling rigs and production wells. This enables operators to analyse data locally, reduce latency and make faster decisions to improve asset performance and reduce downtime.

Ms. Barta, concluded:

“Deployments of wireless IIoT devices with edge computing will be key to optimise assets and improve oil and gas operations.”