IoT Analytics has published a new analysis focusing on smart meters.

It is derived from the comprehensive “Global Smart Meter Market Tracker”. The tracker includes installed base, shipments and shipment revenues for electricity, gas and water smart meters. The current analysis underscores the global adoption rate of smart electricity meters in 2024, providing an in-depth regional exploration and market forecast.

Key insights:

- By the end of 2023, 1.06 billion smart meters (electricity, water and gas) have been installed worldwide, according to IoT Analytics’ Global Smart Meter Market Tracker 2020–2030.

- Smart meters enable utility service providers across the world to digitalize their distribution infrastructure and services efficiently with near real-time data.

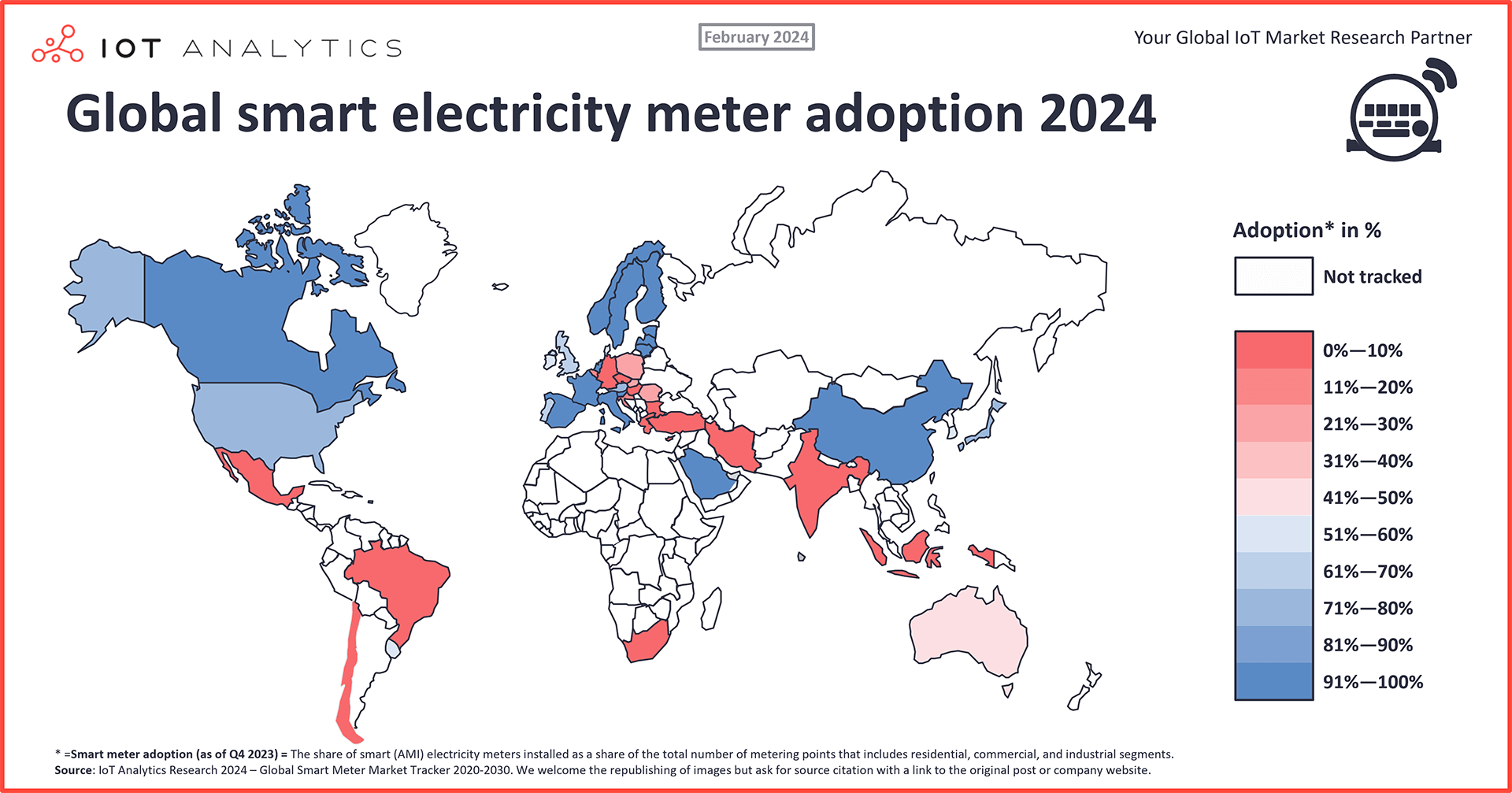

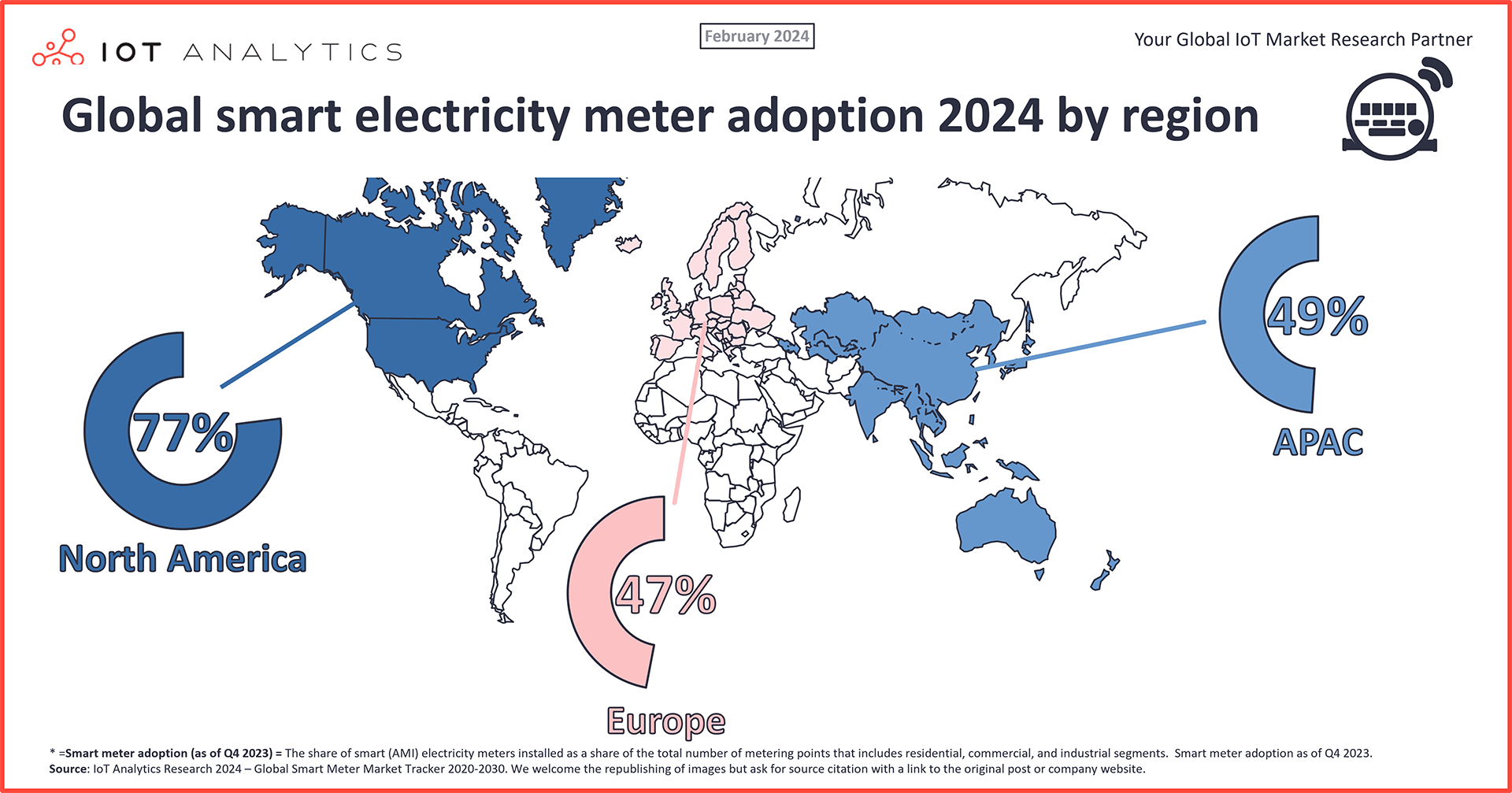

- North America has the most mature smart electricity meter market, with nearly 77% electricity meter market penetration, while Latin America has largely lagged in its adoption of the technology. Some European Union countries and the East Asian region, too, have high rates of smart electricity meter market penetration.

- South Asia, Latin America, and Africa represent a high-growth potential for smart meters, as some regional governments have become convinced of the need to update their aging grid infrastructure and are more actively engaging with smart grid industry stakeholders to develop regulatory policies to drive the adoption of smart meters.

Key quotes:

-

Knud Lasse Lueth, CEO at IoT Analytics, remarks: “IoT-based smart electricity meters have become a reality in the world but adoption varies greatly by country and region with countries like Sweden, France, or Canada having completed or nearly completed their roll-outs while others like Germany are yet to start their initiative in a meaningful way. India is likely to see the largest roll-out in the coming years.”

-

Adarsh Krishnan, Principal Analyst at IoT Analytics, adds that: “Digital transformation is sweeping the utility industry as global service providers’ smart meter deployment, a foundational smart grid technology, exceeds installed base of 1 billion units. While advanced economies embrace feature-rich smart meters, emerging markets focus on more cost-effective solutions for their grid upgrades. Furthermore, future advancements in AI and edge computing will bring greater operational efficiencies and innovative consumer services, creating sustainable and resilient smart grids.”

By the end of 2023, Utility Service Providers (USPs) around the world will have installed over 1.06 billion smart (electricity, gas, and water) meters, according to IoT Analytics’ updated Global Smart Meter Market Tracker 2020–2030. As IoT devices, smart meters are enabling energy and water USPs to build resilience into their operations with near real-time data from their distribution networks. With sustainability and the digitalization of utilities gaining traction worldwide, the installed base of these devices is expected to exceed 1.75 billion by 2030 (CAGR 6%), making the smart meter market a market to watch closely.

Smart electricity meter adoption is far ahead of the adoption of smart gas and smart water meters at this point, though the picture could change by 2030, with smart gas and water meter adoption expected to grow at 10% and 16% CAGR, respectively.

While the tracker provides in-depth coverage of smart electricity, gas, and water meters across 52 countries and 5 regions—including installed base, shipments, revenue, market penetration, and connectivity technology—IoT Analytics plans to offer highlights for each smart meter submarket separately as its own article, starting here with smart electricity meters.

Global smart electricity meter market snapshot

As of late 2023, the smart electricity meter market achieved 43% penetration of the overall global electricity meter market, according to the market tracker.

Electricity grid modernization initiatives started in the late 2000s in Italy and the US and accelerated to national rollouts throughout the EU and APAC regions after 2010. Regulatory policies—supported by financial incentives from regional or national governments—have contributed to this growth, as these policies have encouraged utilities to replace mechanical electricity meters with smart meters to modernize their grid infrastructure.

However, as discussed below, not all parts of the world are modernizing their electricity infrastructure. According to the tracker, North America, Europe, and East Asia have had higher rates of smart electricity meter market penetration, but adoption rates still vary from country to country. Meanwhile, Latin America, Africa, and South Asia have been slow to initiate smart electricity meter projects across the board. Some countries have initiated large-scale smart electricity meter projects in recent years, though project implementation complexity, lack of regulatory policies, and cost hurdles have delayed rollouts in several countries.

Overall, the market for smart electricity meters looks promising, as the Smart Meter Market Tracker forecasts these IoT devices to achieve 54% adoption of the overall global electricity meter market by 2030.

Definition: Smart electricity meters

-

A smart electricity meter is an electronic IoT device used in measurement systems deployed by utility service providers (USPs) to gauge various parameters in distributing electricity to consumers. Smart meters are part of the USPs’ automated metering infrastructure (AMI) systems, which leverages bi-directional communicationthat allows utility head end systems to collect data and communicate with the smart meters.

-

Smart electricity meter features are not limited to real-time consumer usage data; they also include near real-time insights around power quality, voltage fluctuations, and outages in the USPs’ distribution infrastructure.

Smart electricity meter market and adoption by region

While the smart meter market tracker shares market data down to the country level, the following are highlights about the smart electricity meter market at the regional level.

North America leads in smart electricity meter adoption

North America has the most mature smart electricity meter market, with nearly 77% electricity meter market penetration by the end of 2023.

In the US, smart electricity meters have 76% penetration in the overall electricity meter market as of 2023, driven by large-scale deployments from investor-owned utilities. Smart meter rollouts in the US are expected to slow down or plateau during the forecast period due to smart meter’s high penetration rate and long product life cycles. As municipalities with smaller budgets and cooperative-owned utilities replace their traditional electricity meters with smart meters, smart meter annual shipments in the US should see marginal growth through the rest of the decade.

Furthermore, the region will get a further boost in smart meter shipments, as Canadian utilities Fortis and Hydro One have announced plans in 2023 to replace their existing AMI with 2nd-generation smart meters.

The APAC region has the second most mature smart electricity meter market, driven by nationwide deployments in China and Japan.

Meanwhile, the APAC region has the largest addressable market for smart electricity meters, with over 1.1 billion electricity metering endpoints. In 2023, the APAC region accounted for almost 60% of the global smart meter installed base and more than 50% of annual smart meter shipments. In 2023, the region achieved a smart meter penetration rate of 49%, largely driven by successful nationwide rollouts in China and Japan. With planned nationwide deployments in Australia, South Korea, India, Indonesia, and Singapore, the region’s smart meter penetration is expected to reach 67% by the end of this decade.

Of note in this region, in 2021, India’s government set an ambitious goal of installing 250 million smart electricity meters by the end of 2025. To execute the implementation strategy, the government of India launched the Revamped Distribution Sector Scheme (RDSS) not only to help financially support regional USP smart meter deployment and maintenance but also to expand the domestic manufacturing capacity to produce smart meters within India. By the end of 2023, India had achieved less than 3% of this goal, making it unlikely for this goal to be met before 2030. That said, by 2030, India is on track to become the single largest market for smart electricity meters in terms of annual shipment and revenue.

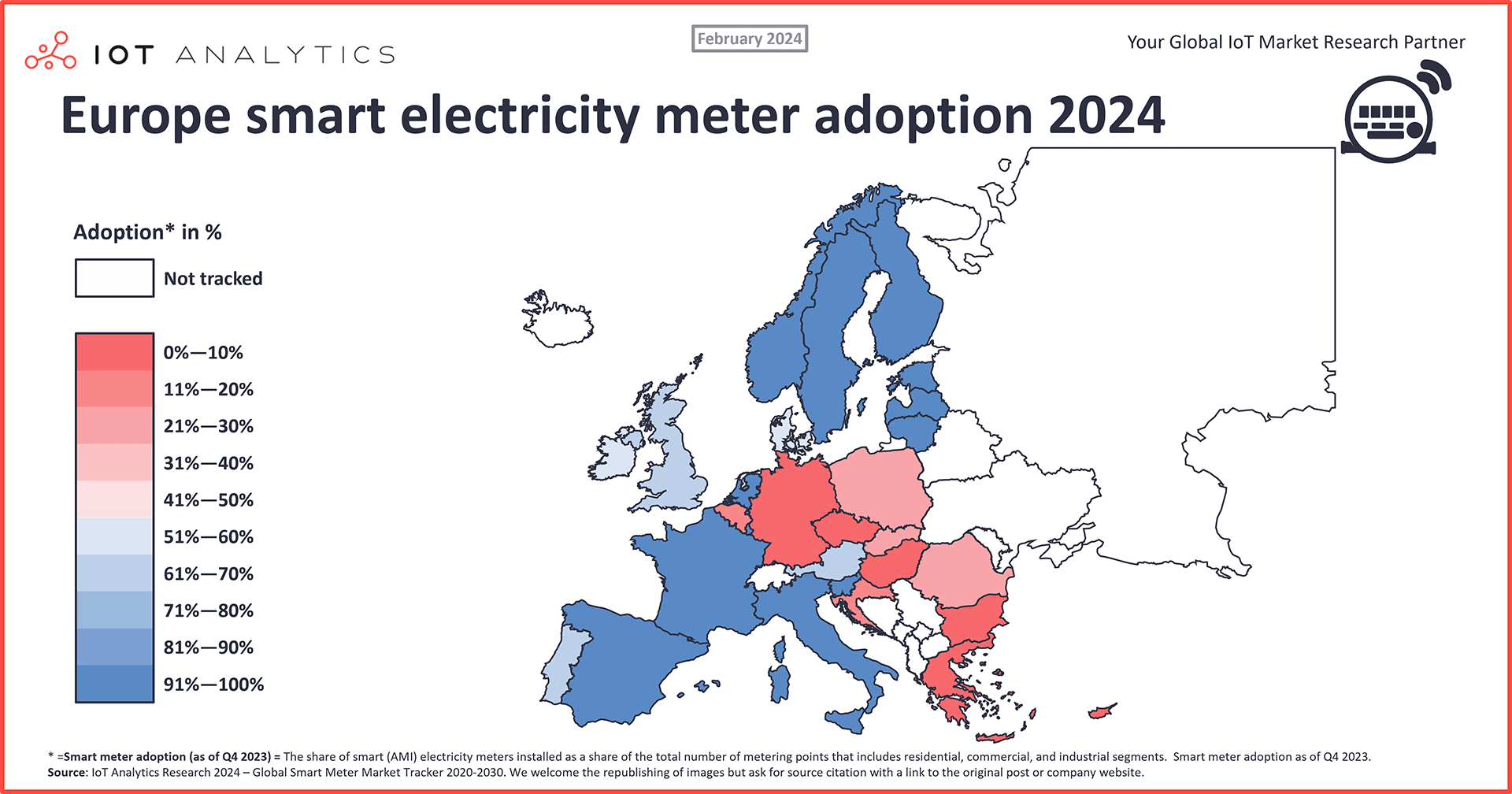

Europe comes third in smart meter adoption, though adoption differs greatly by country

Europe had 47% smart electricity meter market penetration across the continent at the end of 2023. France, Spain, Italy, Netherlands, and the Scandinavian countries initiated nationwide rollouts in the last decade, while Greece, Hungary, Poland, and Romania only started their initiatives more recently.

Germany, with over 50 million electricity metering points, has largely lagged in its adoption rate, with under 10% of smart electricity meters deployed to date. However, in early 2023, the government of Germany revamped its 2016 Metering Point Operation Act to speed up smart meter deployments, targeting a complete rollout by 2032. The new law stipulates binding deadlines for USPs with a roadmap that includes 20% rollout by the end of 2025, 50% by the end of 2028, and 95% by the end of 2030 for residential and small business consumers, with targets extending to 2032 for large consumers. However, there is strong market skepticism around achieving these deadlines due to the need for clarity from the government around financial support for USPs, AMI technical specifications, data privacy, and security governance framework.

Saudi Arabia and the UAE lead in the Middle East and Africa region

In the Middle East and Africa region, Saudi Arabia and UAE are leading the way in the implementation of smart meters for electricity. In 2022, Saudi Arabia’s state-owned USP Saudi Electricity Company (SEC) announced the successful deployment of approximately 11 million smart meters over three years. Meanwhile, the UAE, which already has 1.6 million smart electricity meters installed, is expected to complete its nationwide rollout by the end of 2029.

Latin America lags in smart electricity meter adoption

Finally, Latin America has seen the slowest smart electricity meter deployment, largely due to regulatory indecisiveness delaying project rollouts. Uruguay was the first country in the region to mandate a nationwide smart meter rollout, aiming for completion in 2026.

Analyst’s outlook on the electricity smart meter market

Though regional variations persist—with energy USPs in North America, Europe, and East Asia boasting much more mature markets than their counterparts—the regions of Southern Asia, Latin America, and Africa represent a high-growth potential for smart meters. Some key considerations for various stakeholders are as follows:

- Market saturation and marginal growth in advanced economies: The implementation of more advanced and feature-rich 2nd-generation smart meters is already underway or in the advanced planning stages in countries such as Sweden, Italy, Finland, and Canada. This is likely to marginally drive up the average selling price of smart electricity meters.

- Cost sensitivity in emerging markets: In regions such as South Asia, Latin America, and Africa, where penetration rates are lower, some national governments are convinced of the need to upgrade their aging grid infrastructure and are actively engaging with smart grid industry stakeholders to develop regulatory policies and standards to drive the adoption of smart meters. However, these are also cost-sensitive markets where low-cost smart meters are more likely to be successful.

- Smart meter supply chain diversification: Several countries (e.g., Saudi Arabia, Mexico, Brazil, India, and Indonesia) that are initiating large-scale rollouts are stipulating that smart meter OEMs localize the manufacturing of 40% or more of the smart meter demand.

- Regulatory policy uncertainties: Policy indecisiveness creates complex and uncertain environments for smart meter stakeholders, hindering innovation and investments that subsequently delay smart meter deployments, as seen in countries such as Brazil, India, Mexico, and South Africa.

- Future innovations and market trends: Innovations in ICs, edge computing, and AI (TinyML), as seen in 2nd-generation smart meters, may help reduce strain on communication networks, improve real-time responses to grid fluctuations, build resilience, and enhance data security and privacy.

Based on the Global Smart Meter Market Tracker 2020–2030, the traditional USP industry, once considered a laggard in adopting new technology innovations, is leading the digital transformation market with more than a billion smart meters and accelerating its digital footprint.

IoT Analytics will closely monitor this evolving USP industry and technology landscape to provide in-depth analysis and actionable insights into this market. Its next report on energy utilities (expected in Q2 2024) will provide a deep dive assessment of USPs in 10 countries to identify key trends in smart grid programs, such as distribution automation, green energy integration, and EV charging infrastructure.