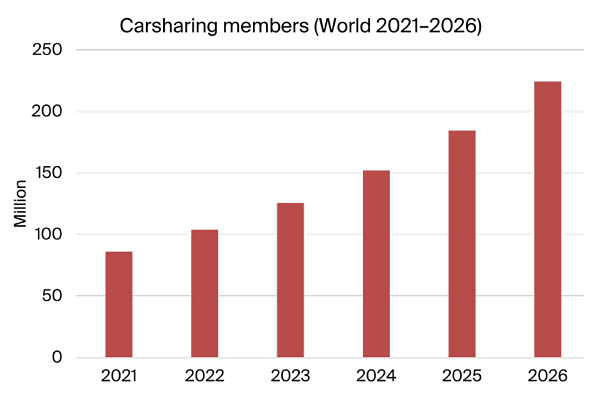

According to a new research report by IoT analyst firm Berg Insight, the number of users of carsharing services worldwide is forecasted to grow from 86.0 million people in 2021 at a compound annual growth rate (CAGR) of 21.1 percent to reach 224.3 million people in 2026.

Berg Insight forecasts that the number of vehicles used for carsharing services will grow at a CAGR of 12.5 percent from 539,000 at the end of 2021 to 973,000 at the end of 2026. The carsharing fleet grew 2.2 percent worldwide in 2021 and performance varied on regional level.

Martin Cederqvist, IoT analyst at Berg Insight, said:

“While the Covid-19 pandemic has created challenges for carsharing operators in China, the European market continues to show good uptake and grew 21 percent in terms of fleet size in 2021.”

The South American and Middle Eastern markets have grown rapidly in the past year. The North American market has struggled in recent years, but partly recovered in 2021 when the total fleet size increased by 16.2 precent while membership decreased by 4.3 percent.

CarSharing Organisations (CSOs) offer members access to a fleet of shared cars 24/7 from unattended self-service locations. Usage is billed by the minute/hour and by distance driven, with rates that include fuel, insurance and maintenance. Today, most CSOs use station-based networks with roundtrip rental. This operational model requires members to return a vehicle to the same designated station from which it was accessed.

Another model that is rapidly gaining in popularity is free floating carsharing, which enables members to pick up and drop off cars anywhere within a designated area. In recent years, a number of CSOs have also experimented with hybrid models of roundtrip rentals and free floating carsharing. Some CSOs also offer one-way carsharing that enables users to return the car to any station operated by the CSO.

“During the COVID-19 pandemic, CSOs adjusted their offers to meet new mobility needs of their customers such as longer rentals, short trips replacing public transport and taxi as well as an increased demand for roundtrip rentals as a replacement for car ownership”, said Mr. Cederqvist.

A connected fleet and specialized software platforms are today necessary to run a carsharing business covering operational activities ranging from management of in-vehicle equipment, fleet management, booking management, billing, as well as operations supervision via dashboards and data analytics. While some CSOs are using in-house developed hardware and software solutions for their operations, the majority sources these kinds of products and services from specialised technology vendors.

Some of the vendors offer an end-to-end solution including both telematics equipment and software platforms while other vendors focus on one of the areas. Leading vendors of hardware and software telematics platforms enabling carsharing services include INVERS, Convadis, Continental, Octo Telematics, Vulog, Mobility Tech Green, Targa Telematics and Glide.io.

Carsharing services are offered by specialist carsharing companies, car rental companies, leasing companies, carmakers, as well as other players such as public transport operators. Examples of leading CSOs owned by carmakers include Free2Move (owned by Stellantis), Volvo On Demand (Volvo Car Mobility), Wible (owned by Kia) and Toyota (Kinto Share).

“In recent years, a few carmakers have exited the carsharing market. BMW and Daimler left the market when they sold their joint venture SHARE NOW to Stellantis in 2022. Similarly, Volkswagen left the market in November 2022 as the carsharing service WeShare was acquired by the German CSO Miles. Stellantis now runs the leading carsharing operator in the car OEM segment Free2Move where SHARE NOW was incorporated in 2022”, said Mr. Cederqvist.

Sixt Share (owned by Sixt), Zipcar (owned by Avis Budget Group) and LeasysGO! (owned by Leasys) are examples of carsharing companies owned by car rental and leasing players. Specialised CSOs include Times Car Plus in Japan, Socar in South Korea, Liandong Cloud and EvCard in China, Enjoy in Italy, Mobility Carsharing in Switzerland, Stadtmobil, Flinkster, Miles and Cambio in Germany, Communauto in Canada and GoGet in Australia.

“The top 25 carsharing service providers accounted for about 71 percent of the carsharing members and managed close to 61 percent of the carsharing fleet worldwide at the end of 2021”, concluded Mr. Cederqvist.